Discovery: Unreasonably Low Expectations

Overview

Discovery, Inc. is an interesting investment at current prices amidst an evolving media landscape. Selling for less than 7x free cash flow, the market is pricing in terminal decline for Discovery’s business. Discovery has taken a different approach to the changing media environment, a path that has so far proven successful. If the management team continues to execute its strategy in traditional linear cable as well as direct to consumer (DTC) segments, annual returns to shareholders could easily exceed 20%. Discovery offers investors the chance to invest alongside famed media “Outsider”, John Malone, who has been a significant buyer of the stock in recent months.

Background

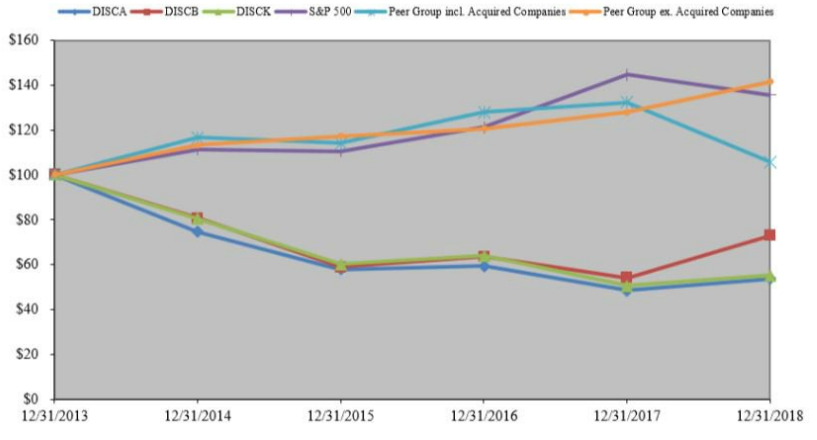

Discovery competes in the media industry against the likes of Walt Disney, Netflix, ViacomCBS, AT&T, and many others. Stocks in this segment have been bifurcated between the haves and the have-nots as cord cutting has accelerated in recent years. A look at a comparison between Discovery and its peer group (legacy linear cable-dependent companies) against Netflix stock performance over the past several years tells the story. Not to compare Discovery to Netflix, but I believe Discovery is being inappropriately discounted which has created an opportunity for long-term investors.

Figure 1: Discovery Stock Performance. Source: Discovery 10K

Figure 2: Netflix Stock Performance. Source: Netflix 10K

Discovery owns several well-known U.S. brands across multiple segments. These include Discovery Channel, TLC, Animal Planet, Investigative Discovery, HGTV, Food Network, and the Travel Channel. Its international brands include Eurosport, DMAX, and TVN. The company operates in over 200 markets worldwide and retains ownership of virtually all content and IP.

Discovery essentially makes money in two ways – advertising and distribution. The company earns revenue from advertising fees for advertising space sold on their networks and digital products as well as from fees charged to distributors (such as cable and satellite companies) to use their first-run content.

Further, the company primarily operates in two segments – linear and direct to consumer (DTC). Its legacy/core business is in linear programming, often referred to as “big bundle” programming, where distributors such as Comcast or AT&T bundle hundreds of channels along with internet offering and charge a significant monthly fee. The company also operates in the nascent direct to consumer segment, commonly referred to as “streaming” of “over the top”. In DTC Discovery offers their content via an app that can be downloaded and accessed on mobile platforms or via devices such as Roku’s, or as a party of “skinny bundles” such as SlingTV. Concerns over the shift from linear to DTC is well publicized and is a primary driver of Discovery’s low valuation. Consumers have been chord cutting at a low to mid-single percentage digit clip in recent years; a trend that is largely expected to continue.

Companies with significant exposure to DTC such as Disney and Netflix have been rewarded accordingly as reflected in their stock prices, while the ViacomCBS and Discovery’s over the world have been seemingly left behind.

Given this changing dynamic, and as John Malone recently pointed out in this interview, the key to long term prosperity for media companies historically dependent on linear is to shift into a hybrid model and begin to monetize the DTC space. I would encourage anyone interested in learning about the dynamics in media to listen to John Malone’s perspective on the current landscape and outlook.

Competitive Position

Despite being lumped in with the “have nots” of the linear network, Discovery possesses a few important differentiators.

The two most critical differences between Discovery and the rest of the linear field are the company’s low-cost content and international presence.

Most media companies are competing in scripted, or fiction, content, which is extremely expensive. In developing scripted content, a provider needs to pay writers, directors, actors, and spend heavily to promote new programs. Netflix and Disney’s are spending billions of dollars annually in this arena. In addition to being expensive the scripted area is highly uncertain. It’s nearly impossible to predict the big winners, the next Game of Thrones for example, and how big those winners will be. Furthermore, consumers in the U.S. won’t necessarily enjoy the same scripted content as those in Europe or Asia, necessitating even more spend and marketing for those wishing to reach international scale. In short – to me there are far too many variables to try and accurately predict outcomes in the scripted content space.

Fortunately for Discovery shareholders, the company has elected not to compete in this area. As CEO David Zaslav said during the Q3 earnings call, “We are not in that series scripted and movie side of the entertainment business. It's crowded. It's aggressive. It's expensive and it's risky.” Discovery produces non-fiction content which costs significantly less to develop given most of the above expenses are drastically reduced. This choice has resulted in industry-leading margins for Discovery as shown below.

Chart 1: Operating Margin Comparison. Source: ValueLine Data and Authors Analysis

Discovery’s content also travels very well and can be recreated at a low cost internationally. In non-fiction, often the only major change needed is to add closed captioning or dub the audio into the local language. From an international standpoint, Discovery has spent the last 3+ decades building out a presence in over 200 markets around the world. Again, as discussed during the Q3 earnings call, the leadership team outlined how important those local connections are to winning in international markets. Discovery has put in the time to build these connections and set themselves up to monetize both linear and DTC globally, and are already beginning to see momentum.

Contrast this approach with ViacomCBS or AT&T (by way of HBO), and there is very little international presence leading to an extreme dependence on the U.S. Higher growth and the associated operating leverage that comes with international economies of scale is also off the table for these businesses.

Growth

Over the past 10 years Discovery has grown free cash flow steadily, as outlined below.

Chart 2: Free Cash Flow Trend. Source: Company 10Ks and Authors Analysis

In order for growth to continue, Discovery needs to find success in both advertising and distribution across linear and DTC segments. The valuation wouldn’t suggest it, but the business is growing now and looks poised to continue in the future.

The management team has outlined that in the U.S. (60% of revenue) revenue should increase at a low to mid-single digit pace this year due to pricing power and monetization of content, along with additional carriage on streaming platforms, which more than offsets cord-cutting pressure.

Internationally, revenue should increase around a 10% clip (currency neutral) due to expansion of digital content and similar pricing power.

The key to sustained higher growth over the longer term appears to be the company’s ability to monetize its DTC offerings. The management team is working in a number of different ways across the globe to make this happen. Efforts include joint ventures with local streaming companies in Europe, the Discovery GO app in the U.S., partnering with Amazon on Food Network Kitchen, and inclusion on virtually every skinny bundle such as SlingTV. When pressed, the management team is careful not to give away too many details because of how new these efforts generally are but reading into their comments provides quite a bit of hope. Last quarter they noted that they are currently monetizing several hundred million dollars of DTC content and over the past few quarters this has started to “meaningfully contribute to revenue growth”.

John Malone seconded this notion both vocally and with his wallet. Malone explained that Discovery “need(s) to make the transition from linear to interactive…and they are reaching out in a number of different ways…and I personally am willing to bet they are going to make this transition”. Malone purchased $75M of shares last year and views the company as dramatically undervalued.

Clearly investing in Discovery involves execution risk, and if the company fails to monetize the DTC segment the business is unlikely to meaningfully grow profits over the long-term. Fortunately, the valuation, discussed below, more than offsets the execution risk.

Fundamentals

Historically Discovery has been a good, but not great, business. Over the past 10 years the company has delivered an average of ~17.5% return on equity. The business has reinvested around 40% of the cash generated from operations and debt and equity issuances. Retained cash has been employed in a mix of capex, content spending, and occasional acquisitions - the largest being the Scripps acquisition in 2018. The remaining 60% of cash inflows have been returned to shareholders via stock repurchases and delevering the balance sheet. The table below summarizes the company’s sources and uses of cash over and return on incremental capital over the past decade.

Table 1: Incremental Return on Capital, 2010-2019 (millions). Source: 10Ks and author’s analysis

The company has returned roughly 15% of incremental capital employed by reinvesting 43% of its cash, leading to an estimated intrinsic value compounding rate (I-ROIC x reinvestment rate) of around 6.5%.

Not surprisingly given John Malone’s significant ownership, the company has been a serious cannibal, repurchasing an average of 5% of shares outstanding (and in many cases a much higher percentage of its market cap) in the years leading up to the Scripps acquisition, upon which part of the deal was funded with stock.

The balance sheet was levered-up to complete the Scripps acquisition, with leverage peaking over 4.5x after the transaction. The company slowed buybacks and focused on delevering to a much healthier 3.1x total debt as of the last quarter. The balance sheet is now investment grade and, given the cash flow profile, a modest amount of leverage is appropriate and enhances returns to equity holders.

Valuation and Forward Returns

Discovery is on track to generate roughly $3B in free cash flow this fiscal year, against a market cap of less than $20B, resulting in a 15% free cash flow yield. Given the company has historically compounded intrinsic value by 6.5% annually, and shareholders will have ~8% of free cash flow available for share repurchases (assuming the company retains 45% of cash flow, slightly higher than average, and returns the rest via repurchases), I think it’s reasonable to expect 15% annual growth in intrinsic value per share.

Turning to the valuation multiple, if the company can show progress towards monetizing DTC and continues to grow free cash flow, a 7x multiple of free cash flow is far too conservative. The market is giving the company little chance to succeed in monetizing DTC content as a 7x free cash flow multiple implies a perpetually shrinking business. Obviously, the management team must execute to deliver these results. Given all the evidence outlined above, the confidence displayed by insiders such as Malone, and the management teams track record, the odds appear quite good. Further, listening to the management team recently, the company is already delivering on DTC initiatives and just needs to continue to do so (they aren’t just selling hope). As soon as they’ve shown clear evidence to the market for a few quarters, a rapid re-rating in valuation would not surprise me.

A business growing at 7% for the foreseeable future should be worth at least the market average, and to be conservative I’ll apply a 10x free cash flow multiple. Table 3 outlines the total expected annual return between growth, benefit from repurchases, and an eventual multiple re-rating.

Table 2: 5-Year Forward Returns. Source: Data from 10K’s, Author’s Analysis

Risks

The biggest risk to this investment is failure to adequately monetize DTC content and being left with a shrinking linear viewer base. This is a real risk but given the company’s global footprint, abundance of free cash flow, experienced management team, pricing power in linear, and early progress against this initiative, I think the odds are favorable. Only time will tell. This risk is also more than offset by the valuation. At 7x free cash flow the bar is set very low, and even amidst failure on the DTC front the 15% free cash flow yield puts a high floor on the long-term share price.

Another risk is that one of the large players (Netflix, Disney, etc.) makes the move from mostly scripted content into non-scripted to compete with Discovery. While plausible, none of the players have shown much of an interest in this area, presumably preferring to swing for the fences in hopes of scripted content home runs. Also, Discovery has built a major lead internationally providing a nice buffer against a new entrant. As the management team highlighted during the November call, the company has spent over three decades building local relationships that are vital to success internationally. These relationships cannot be built overnight.

Conclusion

Discovery is a good, growing company run by a shareholder friendly management team and generating significant free cash flow while sporting an investment grade balance sheet. The current valuation allows investors to buy into this business alongside legendary media investor John Malone for around half-price. While risks are present, the current valuation provides a solid floor for shareholders and presents an investment with asymmetric upside.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.