NortonLifeLock Looks Like A Classic Special Situation Mispricing

NortonLifeLock is a classic Greenblatt special situation: it sold its struggling enterprise division to reveal the wonderful consumer franchise hidden in its shadow. The restructuring has a lot of moving parts and the accounting is messy and will continue to be for the next twelve months.

Investors should skate to where the puck is going, not where it is now. When the dust settles, GAAP accounting will show the company trades at just an 8.6x P/E multiple (net of the upcoming special dividend), and enjoys 50% operating margins.

NortonLifeLock, formerly known as Symantec, recently sold its enterprise security business to Broadcom for $10.7 billion in cash. Net of taxes, NortonLifeLock cleared $8.2 billion. This represents 50% of the company’s current market cap but only 10% of its operating income. Broadcom bought Symantec’s enterprise business for 36 times operating income.

NortonLifeLock, the RemainCo, plans to distribute 100% of the after-tax proceeds via a $12 special dividend in Q1. This will be a return of capital and investors will not be taxed.

Historically, Symantec ran the RemainCo business to maximize profitability, not growth. They milked it for cash to reinvest in their enterprise division. NortonLifeLock has been neglected and under-invested in. Going forward, that will change. Management has a “renewed vigor” and will focus on both growth and profitability.

The market hasn’t caught onto it yet, though. Usually special situations like this occur because of a spin-off, but not this time. There was no Form 10-12b to alert the usual spin-off crowd, and it is largely flying under the radar. Further, NortonLifeLock has a lot of moving parts that are obscuring its underlying value.

Name change from Symantec to NortonLifeLock

Ticker change from SYMC to NLOK

A huge special dividend ($8.2 billion or $12 per share)

A 67% increase in the regular dividend from $0.30 to $0.50, annualized

A $1.6 billion buyback authorization (10% of the current market cap and 20% of the ex-special-dividend market cap) to be completed in the next 12 months

A new CEO, President, and CFO

A reshuffled, smaller, Board of Directors

$1.3 billion of stranded costs to be removed in the next 12 months at a cost of $0.9 billion, funded by asset sales

Over the next 12 months, NortonLifeLock will return $10.3 billion to investors - an $8.2B special dividend, $1.6B of buybacks, and $0.3B of regular dividends. This is 64% of NortonLifeLock’s current market cap.

In short, this is an above average company at a below average price that will pay investors generously in the coming year.

Stranded Costs

The crux of this opportunity lies in NortonLifeLock’s stranded costs. Stranded costs are costs that did not transfer to Broadcom and will not be needed to support NortonLifeLock (Q2 Call). These costs are obscuring the RemainCo’s profitability.

Management identified $1.3 billion of stranded costs that they can eliminate within the next 12 months. There are three categories of costs:

People - Several positions are unnecessary after the sale to Broadcom. The positions will be kept for the next six months to support Broadcom’s transition and then eliminated.

Facilities - Buildings will be sold as positions are eliminated. This process should be completed in 9 months.

Contracts & Other Assets - These odds and ends will be renegotiated or written down. Next quarter will see the heaviest activity for write-downs.

Management estimates it will cost them $900 million to eliminate these stranded costs. The plan is to self-fund this expense. NortonLifeLock already sold its equity investment in DigiCert for $387 million. It expects to generate an additional $700 million from the sale of underutilized real estate. All in all, this will fund the cost reduction program and generate $200 million of excess capital that can be redeployed into direct-to-consumer advertising to kick-start growth.

Current Run-Rate Performance

Management is guiding for $1.50 of EPS next year and $900 million of FCF. Excluding the special dividend, NortonLifeLock sports an $8 billion market cap, which makes it exceptionally cheap if management can deliver.

A look under the hood suggests that they can. In their fiscal 2020 Q2 call, management said the RemainCo business is on track for $1.40 of EPS right now. They expect to grow from $1.40 to $1.50 by removing stranded costs and executing the buyback authorization.

It seems reasonable that their buyback can get them from $1.40 to $1.50 in a year. But is the business really at a $1.40 EPS run rate today? The most recent quarter GAAP EPS were at a $0.70 annualized run rate.

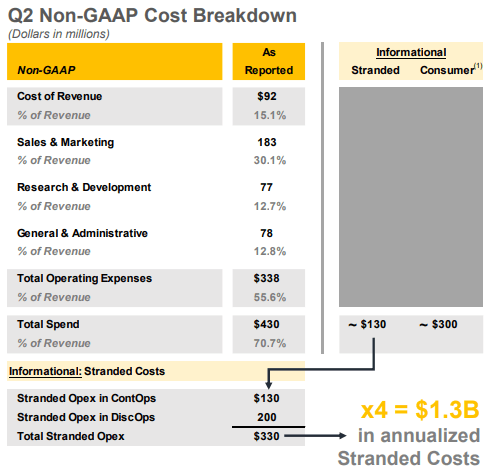

Source: Fiscal 2020 Q2 Presentation

The most recent quarter showed revenue of $600 million and total spend of $430 million for a 28% operating margin. But this includes $130 million of stranded costs. So, the business should be producing $600 million of revenue on just $300 million of spend for a 50% operating margin.

Operating income of $300 million equates to $0.45 of EPS or $1.80 annualized, leaving $0.40 for interest and taxes. All-in-all, management’s math checks out. So long as management can remove the stranded costs, the business ought to show GAAP EPS of at least $1.40 of EPS in a year.

KPIs And Growth

At its core, NortonLifeLock is a simple subscription business. The graphic below, from their fiscal 2020 Q2 presentation, shows that their revenue is a function of their direct customers times the average revenue per user plus partner revenue. Currently, NortonLifeLock has an 88% customer retention rate, which suggests customers have a large lifetime value.

Source: Fiscal 2020 Q2 Presentation

Historically, the business was used as a cash cow, milked for money to spend on the enterprise division. According to CEO Vincent Pilette in the Q2 call:

The business was really run to maximize the profit. And since August, we've not only reinvested some of the incremental savings into marketing activities, but we started deep, weekly operational reviews with Samir, and we focused solely on developing growth opportunities, not just on maximizing profit.

This explains why the business hasn’t grown recently. Customer count has declined while ARPU has grown, largely offsetting. Customer count showed signs of stabilizing in the most recent quarter.

Joel Greenblatt talks about how spin-offs unleash pent-up entrepreneurial forces. That seems to be occurring here. As Mr. Pilette said on the most recent call:

We have a renewed vigor as we focus on the Consumer business with a sole objective to solidify our growth plan to return the business to mid-single-digit revenue growth in the long term.

NortonLifeLock has a couple of levers to pull for growth. One is to increase the number of subscribers. They plan to spend 1-2 points of margin on direct marketing to pursue this. Longer term, they expect to expand to developed markets overseas. Another lever is to increase ARPU by cross-selling and upselling. The recent uptick in ARPU is the result of upselling users into their cyber safety membership programs.

Importantly, NortonLifeLock’s growth will require minimal capital. It will be high-margin and high-ROIC. Growth will also likely leverage the company’s fixed-costs and produce operating leverage.

Even more importantly, as my valuation shows below, NortonLifeLock does not need to grow to be a successful investment. That’s the beauty of paying less than 10x earnings for a capital-light business. Any growth that materializes is simply the icing on the cake.

Valuation And Forward Return

NortonLifeLock plans to pay a $12 special dividend in Q1 (their fiscal Q4). The stock currently trades for $24, which implies its continuing operations are worth $12 per share or $8.0 billion.

Assuming $1.40 EPS, NortonLifeLock is valued at just 8.6x PE and just 8.0x if management delivers $1.50 of EPS next year. This is cheap by any measure.

NortonLifeLock has $1.8 billion of cash and short-term investments against $4.5 billion of debt. Net, that’s $2.7 billion of debt. $1.40 EPS equates to $0.9 billion of net income, which is plenty to comfortably service interest payments. Management recently refinanced their debt to extend maturities for even more comfort.

Though NortonLifeLock’s valuation is attractive, its capital allocation plan is what really caught my eye. When the Broadcom deal closed, NortonLifeLock increased its regular dividend 67% from $0.30 annualized to $0.50. After the special dividend, that’s a 4.1% yield. Further, the board authorized a $1.6 billion buyback which represents 20% of the ex-special-dividend market cap. Together, Norton LifeLock’s 2020 net payout yield will be around 24%.

Once the stranded costs are removed, NortonLifeLock will screen cheap on a GAAP basis and won’t trade at 8x PE for long. It could easily trade at 13x, as management mentioned in their fiscal Q1 call. Then CEO Rick Hill said:

The $8.2 billion after tax proceeds is roughly the equivalent of $12 per share. We believe that post the 12 month transition period as a standalone company, our Consumers Cyber Safety business can generate a $1.50 in non-GAAP annual earnings per share.

Now you apply a multiple of 13 to that number, add it to the $12 per share we are getting for our Enterprise Assets and you get a share price in excess of $30 a share for Symantec. Now obviously, a stable dividend generating company in a low interest to negative interest rate environment would clearly garner higher than a 13x multiple.

A 13x multiple makes sense - that’s the terminal multiple of a DCF using a 10% discount rate and a 2% growth rate. A 13x multiple on $1.40 in 3 years implies an 8% stock CAGR. Adding the 4% dividend yield brings the total return to 12%.

But as Mr. Hill mentions, a 13x multiple is probably overly conservative. The market’s median multiple (17x according to Value Line) might be a better reference point. That implies a three-year total return of 19%.

These scenarios assume zero growth and no buybacks. They rely simply on management cutting expenses, paying their declared dividend, and a multiple re-rating. Any growth or buybacks, like the $1.6 billion authorized buybacks, will add to this return.

What if the stock doesn't re-rate? That's okay - the business is highly cash generative and the Board of Directors (discussed below) is shareholder-friendly. Management targets $900 million of free cash flow next year. If the stock remains cheap, I would expect the Board to authorize another large repurchase. Investors will either profit from a high net payout yield or a re-rating of the earnings.

Management And Insiders

Starboard Value bought a 5% stake in Symantec in August 2018 and today owns 7%. They began agitating for change and nominated 3 representatives to the Board of Directors - Rick Hill, Dale Fuller, and Peter Feld. In May 2019 Rick Hill was named interim CEO and he quickly negotiated the enterprise division’s sale to Broadcom.

Now Mr. Hill’s work is done and on November 8, NortonLifeLock announced another reshuffling of managers and its Board of Directors.

CFO Vincent Pilette will replace CEO Rick Hill. Samir Kapuria will become President and Matthew Brown will become the interim CFO.

Dale Fuller, Rick Hill, David Mahoney, Anita Sands, Dan Schulman and Suzanne Vautrinot will retire from the Board of Directors. CEO Vincent Pilette and Nora Denzel will join the board. Nora Denzel was one of the five directors Starboard Value originally proposed in 2018.

At the end of the day, Starboard will still have two directors on the board: Mr. Feld, who is Starboard’s head of research, and Ms. Denzel, who is a director at AMD, Ericsson, and was an executive at Intuit. The board also has managing directors from Silver Lake Partners and Bain Capital. This should ensure efficient capital allocation remains a priority.

Historically, NortonLifeLock has incentivized managers with Performance-based Restricted Stock Units (PRUs). The payout is equal-weighted with respect to annual EPS, annual FCF, and 3-year total shareholder return versus the Nasdaq 100.

This isn’t the best incentive comp program I’ve seen, but it’s not the worst. It should be sufficient to align management’s interests. I’m more reassured by Starboard’s continued skin-in-the-game and happy they continue to have a few seats on the board.

Risks

The primary risk I see is execution risk - can the stranded costs be as easily removed as promised? Will they prove more costly or time-consuming to remove?

CEO Rick Hill came in and retooled the company in a matter of months. He’s leaving a plan and momentum in place. But can the new CEO execute it? I’m comforted that the new CEO was the former CFO. He’s a veteran, not an outsider, and should know the company and the plan well.

There’s also a risk that the company cannot self-fund the expenses to remove the stranded costs. The self-funding plan revolves around real estate sales, which can be fickle. NortonLifeLock is under-the-gun to remove the stranded costs in the next twelve months and might be forced to sell some real estate and a lower-than-assumed price to free up capital. Luckily, asset dispositions are forecast to produce $200 million in excess of what’s required to remove the stranded costs. This provides a margin of safety.

A further mitigant is the new CEO’s self-proclaimed conservatism. On the fiscal Q2 call he said: “Proceeds received from sales of underutilized assets keep going up as we are conservative in our projections and only want to make sure we forecast where we have line of sight, too.” Indeed, management did reduce the forecast amount of stranded costs and increase the forecast asset-sale proceeds between fiscal Q1 and Q2.

Summary

NortonLifeLock is undergoing a lot of change. Its financials are messy, and will continue to be for the next twelve months. But management has a credible plan to remove stranded costs. In doing so, next year’s GAAP earnings will showcase the quality of the remaining business. Investors get paid to wait with a large buyback and increased dividend. Meanwhile Starboard Value continues to remain invested and keep the company focused on efficient capital allocation.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.