A&W Revenue Royalties Income Fund

A&W Revenue Royalties Income Fund is a Canadian-listed small cap fund that operates as a “skim off the top” business for all Canadian A&W Restaurants.

Separated from its American counterpart in 1972 and bought out by management in 1995, A&W operates the second largest burger chain and the fifth largest overall restaurant brand in a consolidated Canadian QSR industry.

Source: 2019 Annual Report

A&W maintains a strong and growing brand with bright prospects. The operating business (A&W Food Service of Canada) is privately owned, but investors can participate in the growing franchise by way of owning A&W Revenue Royalties Income Fund on the Toronto stock exchange.

Before diving in to the details, I want to credit Max from Kaho Partners for the introduction to this business. Kaho is a private investment firm primarily focused on acquiring wholly-owned businesses. Matt and I periodically collaborate and exchange ideas with Max and Griffin, Kaho’s principals. They put out great material and I’d recommend checking out their website for some interesting reading.

Structure

A&W Revenue Royalties Income Fund (the Fund) owns the rights to the A&W trademark by way of its ~75% ownership in the entity A&W Trade Marks, with the other ~25% being owned by A&W Food Services (the operating company). The Fund currently owns the rights to the A&W trademark for the next 80 years through 2100.

In exchange for using its trademarks A&W pays the Fund 3% of revenue from all A&W restaurants in the royalty pool, which is adjusted each year to include revenue from new restaurant locations, net of any closures. The Fund enjoys a powerful economic model. They incur virtually no costs and require no capital to grow. Subsequently this allows the Fund to pay out nearly 100% of a growing cash flow stream each year to unitholders.

Without getting too far into the weeds, to reward A&W Food Service for growing the restaurant base, the Fund basically pays Food Services an amount equal to the royalty fee generated by new locations from the previous year capitalized at the Funds current yield. The payment is made in shares and increases Food Services’ interest in the Fund each year. This effectively offsets the impact from new location royalty revenue to current Fund unitholders. I’ll review the economic impact of this arrangement later.

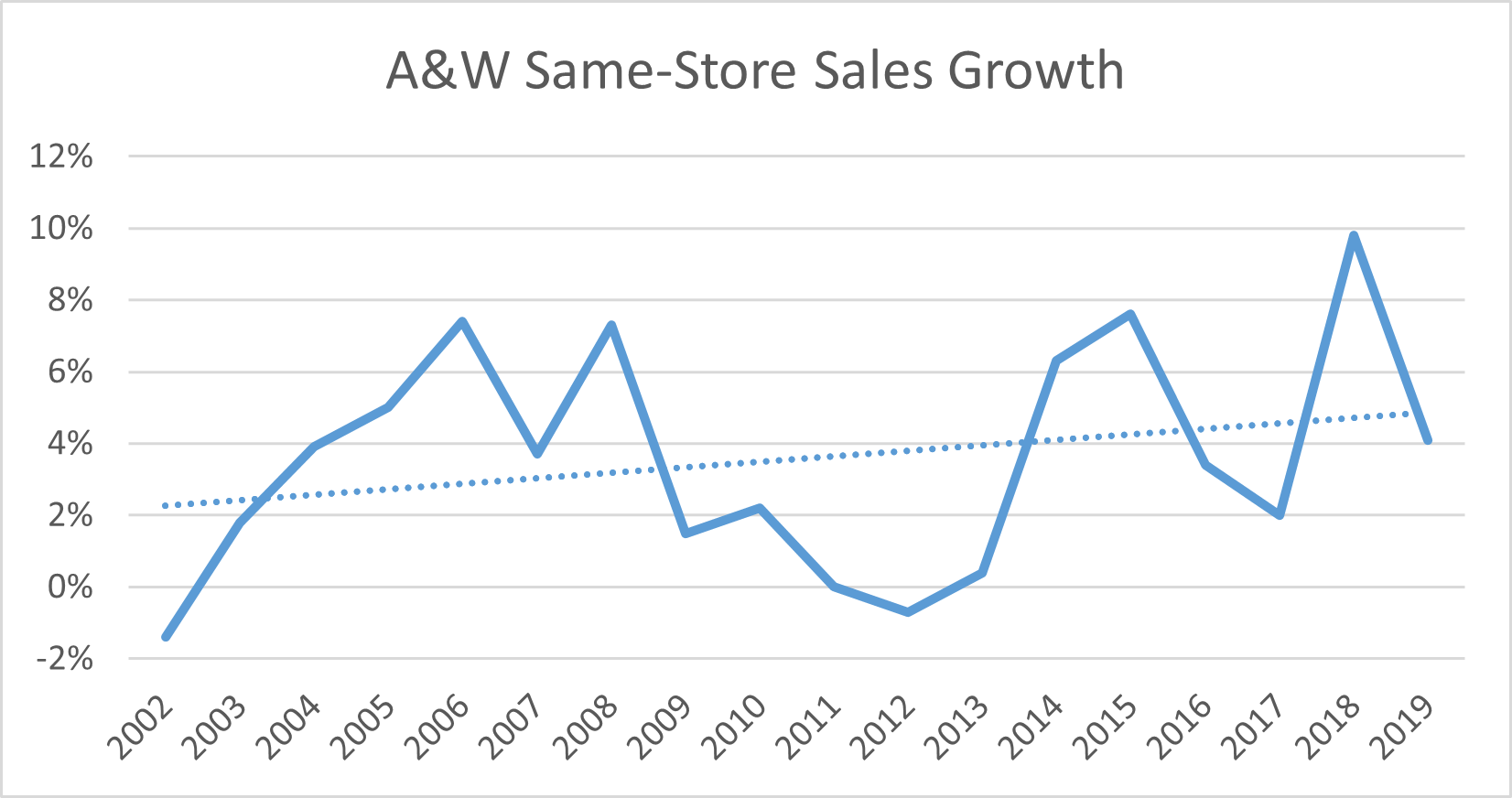

Growth

A&W enjoys a dominant position in a growing QSR industry and has a resilient track record of growing same-store sales. Since the Fund went public in 2002 A&W has averaged roughly 4% annual same-store sales growth.

Source: Author, company filings

Of note, A&W has only experienced two years of negative same-store sales, once in 2002 and again in 2012. Each of these years growth was only -1%.

A&W has done a superb job leaning in to consumer trends and building a strong brand. In 2013 they became the first QSR chain to offer only beef raised without hormones or steroids and in recent years they’ve been early adopters of plant-based offerings, a mobile app, and pickup and delivery offerings. Management stresses a customer-first mindset and better quality ingredients. This has resulted in an impressive 5.5% average same-store sales growth since 2013.

Like same-store sales, A&W locations have also grown steadily for years.

Source: Q2 Investor Presentation

Growth in same-store sales and number of restaurants has resulted in an ever-growing revenue pool for the Fund.

source: 2019 Annual Report

Given the near-zero cost structure of the Fund, distributable cash has grown at the same pace as royalty pool gross sales, or roughly 10% annually for the last several years.

As mentioned above, the fund pays Food Services in shares for revenue from new restaurants in a way that amounts to share count dilution that offsets increased royalty revenue from new locations. The net result is distributable cash per share (what matters to Fund investors) basically grows at the same rate as same-store sales, which has averaged 4% over long periods of time and 5-6% in recent years.

Source: company flings, Author

So, 10% annual growth in royalty revenue (from same-store sales growth and new units) partially offset by annual share count dilution of 4% has resulted in distributable cash per growing ~6% annually from 2014 - 2019. Since 2002 distributable cash per share has grown 4% annually, almost the same as same-store sales, as expected.

Despite years of healthy growth, it appears A&W has plenty of runway left in Canada. McDonald’s operates over 1,400 locations (and counting) in Canada compared to less than 1,000 for A&W and management intends to continue expanding A&W’s footprint. Also, Canadians continue to eat our more frequently than previous generations yet still eat away from home far less than the average American, leading to an opportunity for increased penetration.

Source: 2019 Annual Report

Given the attractive economics of the Fund and the solid underlying base business, it isn’t surprising that Fund unitholders have enjoyed excellent total returns over the years, trouncing Canadian stock market benchmarks since 2002.

Like most businesses, however, shutdowns from the pandemic have temporarily set back A&W’s business and provided an opportunity for long-term investors.

COVID-19 Impacts

As Canada’s economy ground to a halt this past spring, so did A&W’s revenue. When royalty revenue temporarily disappeared, the Fund suspended distributions until the situation stabilized, which it did fairly quickly. During the second quarter, same-store sales dropped over 30%. During the third quarter, same-store sales were off roughly 13%, but only 7% over the last few weeks of the quarter. It appears likely that, barring another major shutdown, A&W should be back to pre-COVID levels in the near future, likely sometime in 2021.

After suspending distributions briefly the Fund reinstated monthly distributions in July. Current distributions stand at roughly $1.20/share compared to $1.90 before the lockdowns.

The stock has yet to recover as rapidly as same-store sales. Recently, shares in the Fund were still around 30% lower than pre-COVID levels and 40% off 2019 highs. At recent prices shares trade at or below 15x normalized earnings, seemingly too cheap for an asset of this quality. It’s likely the small size (~$300M market cap), foreign listing, and temporarily depressed distribution are impeding investors from rationally pricing the stock by considering its long-term prospects.

Taking a step back and looking past the pandemic paints a different picture. Large QSR chains are poised to emerge from the pandemic-induced recession in a much stronger relative position. As mom-and-pop restaurants lack the resources and capital to weather dramatic downturns, larger chains should gain market share as consumers return to a normal eating out pattern in the not too distant future. Better mobile and delivery capabilities compared to competitors accentuate their advantage. This could lead to better same-store sales trends and higher distributable cash for A&W in the coming years.

If sales are recovering and a path back to $1.90 per share in distributable earnings seems likely, it appears there is a disconnect between the price of the stock and the value investors are likely to receive over the coming years. The question is, how big is the gap?

Valuation and Returns

A&W Revenue Royalties Fund represents a growing, high-quality, defensive cash flow stream supported by a durable QSR brand. The Fund requires no capital to grow cash flow and benefits from the investments of others. What should that be worth to investors?

If the next 5+ years looks like the past 20 and the company can steadily grow same-store sales at 4-6% annually, the stock should be worth somewhere between 17x – 26x distributable cash flow (more technically, this represents a terminal value based off of 4-6% growth at a 10% discount rate), materially higher than where the stock has recently traded. A 17x valuation may well prove conservative considering the high-quality nature of the business, not to mention the current interest rate environment. It seems probable that a business like this is valued more like a high-quality bond (that also grows) in the coming years, which would suggest a much higher valuation than the market is assigning to the stock today.

When A&W returns to 2019’s sales levels, investors in the Fund will enjoy a ~6.5% base yield (2019’s distribution per share compared to recent market prices) that should grow at 4-6% annually for several years, representing an 11-13% base return before any benefit from the aforementioned valuation re-rating. Putting a low-20s out-year valuation multiple on distributable cash flow, total stock returns could reasonably be 15-20% annually for several years from prices observed in recent months.

Disclosure: The author, Eagle Point Capital, or their affiliates may own the securities discussed. This blog is for informational purposes only. Nothing should be construed as investment advice. Please read our Terms and Conditions for further details.